Bed and ISA is the most widely used, most poorly documented piece of year-round housekeeping in UK financial advice. At the mechanical level it is simple: sell a holding in a General Investment Account, rebuy it inside the client's ISA, and future growth is sheltered from CGT and income tax. At the advice level it is not simple at all. The CGT annual exempt amount has shrunk from £12,300 in 2022/23 to £3,000 in 2026/27, which means the crystallised gain on a typical "bed" step now very often exceeds the allowance and triggers a real tax charge. The suitability case has changed with it. This guide walks through the bed and ISA mechanic, the CGT interaction in the 2026/27 tax year, when and how to run it across the year, and what the file needs to show.

What "Bed and ISA" Actually Means

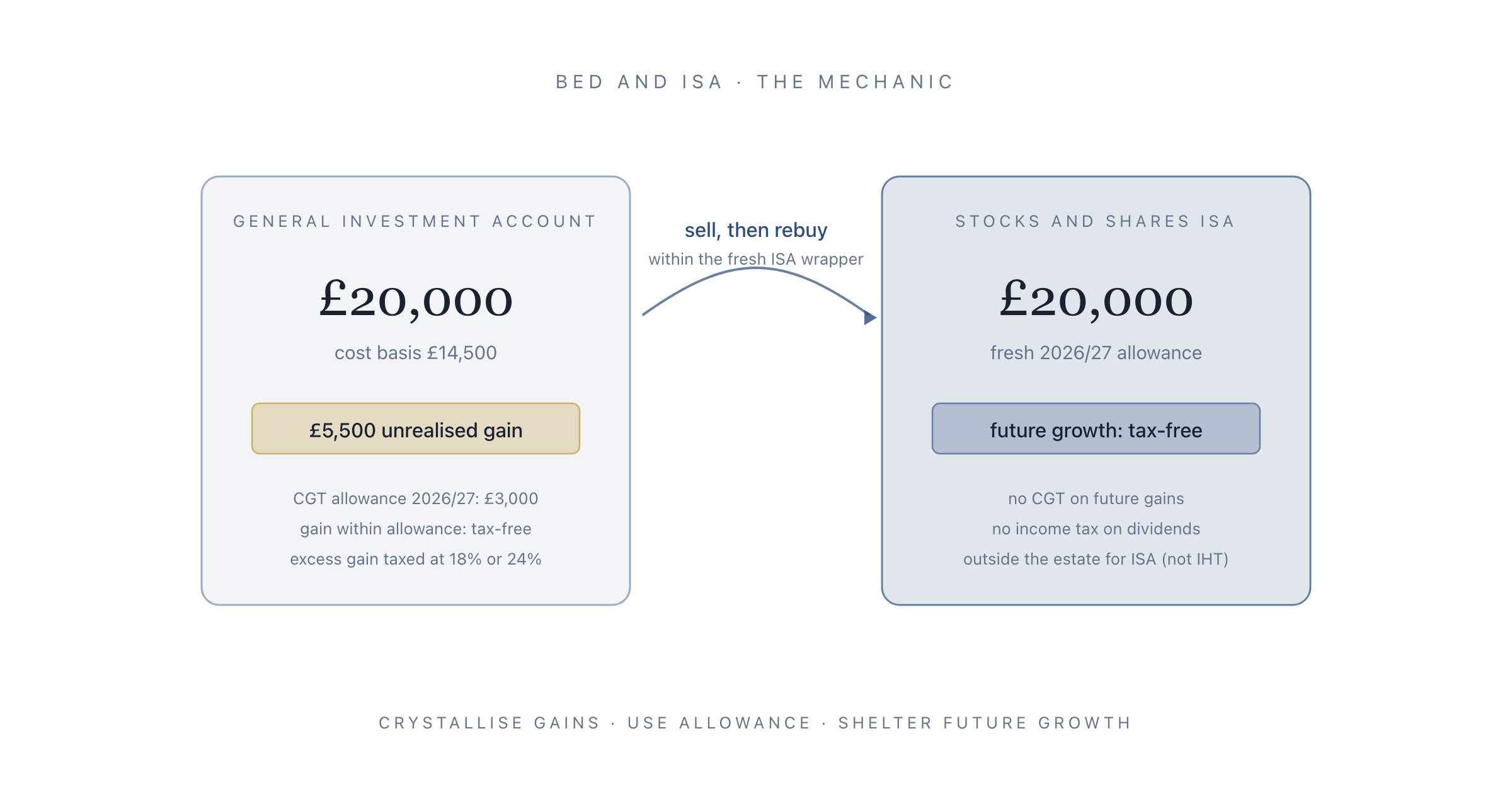

The name is a relic. Before 1998, the common phrase was "bed and breakfast": sell a holding on Friday, buy it back on Monday morning, crystallise the gain, reset the cost basis. HMRC closed that loophole with the 30-day share-matching rule, which now requires a 30-day gap between sale and repurchase of the same security in the same account if the disposal is to crystallise a gain for CGT.

"Bed and ISA" survives the share-matching rule because the repurchase happens inside the ISA, which is a different tax wrapper. For share-matching purposes, the General Investment Account and the ISA are treated as separate holdings, so the sell-and-rebuy can happen on the same day without triggering the anti-avoidance rule. The mechanic:

- Sell. The client sells units of a fund (or shares, or an ETF) in their General Investment Account. The disposal crystallises any unrealised gain against the sale price.

- Transfer. The cash proceeds move into the ISA wrapper as a fresh ISA subscription, up to the annual allowance (£20,000 for 2026/27, unchanged).

- Rebuy. The same holding is repurchased inside the ISA, usually at the next available dealing point. Most platforms offer a single "bed and ISA" button that handles all three steps as a linked transaction with a tight pricing window.

The outcome: the client ends up holding the same economic exposure, but the holding is now inside a tax wrapper that shelters future growth and dividends.

Why the CGT Allowance Change Matters

The case for bed and ISA has strengthened, not weakened, as the CGT annual exempt amount has fallen. Over the last four tax years:

- 2022/23: £12,300

- 2023/24: £6,000

- 2024/25: £3,000

- 2025/26: £3,000

- 2026/27: £3,000

An allowance of £12,300 meant many GIA holdings could be quietly bedded into the ISA each year without any CGT charge, because the crystallised gain fell within the allowance. At £3,000, most meaningful holdings breach the allowance, and the bed and ISA conversation becomes a conversation about realising a taxable gain deliberately, in a controlled way, in exchange for moving the asset into a permanent tax shelter.

That framing change is the single most important update to the adviser's bed and ISA case. Pre-2023, it was administrative housekeeping. Now it is a deliberate tax crystallisation decision. The file needs to reflect that.

The Arithmetic, with a Worked Example

Take a client with £40,000 in a General Investment Account, purchased at a cost basis of £29,000, for an unrealised gain of £11,000. The client has £20,000 of fresh ISA allowance available for 2026/27 and has used no CGT allowance so far this tax year.

If they bed the entire position into the ISA in a single tax year:

- Sale proceeds: £40,000. Gain crystallised: £11,000.

- CGT allowance absorbs £3,000 of the gain. Taxable gain: £8,000.

- Tax charge at 18% (basic rate) or 24% (higher/additional rate) on the £8,000. That is £1,440 to £1,920 of actual CGT.

The client is paying up to £1,920 of CGT today to shelter a £20,000 position plus future growth and dividends. Whether that is good advice depends on:

- The expected holding period (longer = more CGT saved over time, better deal).

- The expected total return of the holding (higher = more to shelter, better deal).

- The client's marginal CGT rate this year versus in future years (lower now = better time to crystallise).

- The interaction with dividend tax (fund has high distributions = ISA shelters more).

The naive conclusion from a spreadsheet is almost always "yes, bed the full £20,000 this tax year, eat the CGT, lock in the shelter." The real conclusion is almost always "split the bed across two or three tax years so the crystallised gain sits closer to the annual allowance each year." The CGT saved by splitting compounds over time, because the annual allowance resets.

The Three Windows in the Tax Year

There are three natural windows in which bed and ISA conversations happen. Each has different framing.

Window 1: Start of the Tax Year (April to June)

This is where we are now. The 2026/27 tax year opened on 6 April 2026. The fresh £20,000 ISA allowance is available. The fresh £3,000 CGT allowance is available.

Running bed and ISA early in the tax year gives the client eleven-plus months of tax-free growth inside the ISA wrapper, which can be worth more than people think. It also avoids the end-of-year rush, when platforms can miss the 5 April cut-off due to volume.

Suitability note: early-year bed and ISA requires the adviser to be confident the client will not want to use some or all of the ISA allowance for other subscriptions (fresh cash contributions) later in the year. If the client reliably adds cash to the ISA in the autumn or winter, an early bed and ISA might crowd out that contribution.

Window 2: Mid-Year Rebalancing (September to November)

The middle of the tax year is when most advisers run their formal client reviews. For clients who have both a GIA and an ISA, the annual review is a natural moment to run a bed and ISA as part of the wider rebalance. The advice logic: if we are going to sell part of the GIA anyway to rebalance back to the strategic asset allocation, let us run the sale as a bed and ISA rather than a taxable disposal with no wrapper benefit.

This is also the window in which the CGT calculation is cleanest. The client has usually made no other disposals during the tax year so far, so the £3,000 allowance is still available in full. The adviser can model the taxable gain precisely.

Window 3: End of the Tax Year (February to Early April)

The classic window. Use the expiring ISA allowance before 5 April, or lose it permanently.

The risk of running bed and ISA only in this window: platforms can slip their deadlines due to volume. Many platforms set an internal cut-off of late March for bed and ISA requests to guarantee the transaction will settle before 5 April. If the adviser submits in late March and the trade does not settle until 7 April, the subscription counts against the new tax year's allowance instead of the old one.

For clients who come through the door in late March, the safer adviser answer is often "we will run this in the new tax year starting 6 April, and use the fresh allowance." That is the same outcome, without the platform-deadline risk.

What to Document in the File

The Consumer Duty and the broader suitability regime both require the adviser to document not just what was done but why. For bed and ISA, the file should show:

- The tax context. Current tax year allowances (CGT £3,000, ISA £20,000), client's marginal CGT band, any CGT already used this tax year from other disposals.

- The quantitative case. Expected CGT payable on the crystallised gain, estimated ISA shelter value over a reasonable planning horizon (5 or 10 years is conventional), and the break-even point where the shelter saving exceeds the CGT paid.

- The alternatives considered. Splitting the bed across multiple tax years, deferring entirely, using a pension contribution instead, or doing nothing. Each alternative gets a brief comparative.

- The client's preference. The conversation in which the adviser walked through the options and the client chose. This is the bit most files miss. Bed and ISA is a joint decision, not a mechanical recommendation.

- The post-execution confirmation. Trade confirmations, the new ISA subscription amount, the new cost basis inside the ISA, the crystallised gain for the SA100 return next year.

The first three items belong in the meeting notes for the review at which the decision was made. The fourth is the single most important evidence point for Consumer Duty, because it is the one that demonstrates "Consumer Understanding" was actually achieved. The fifth lives in the back-office workflow rather than the advice file, but the adviser should be able to retrieve it if the FOS or an internal compliance review asks. For a fuller walkthrough of how Consumer Duty applies to decisions like this, see our guide to the four Consumer Duty outcomes.

The Conversations Advisers Miss

Three bed and ISA adjacent conversations show up in review meeting notes across the industry, and most files handle them imperfectly.

The Spousal Angle

Married or civil-partnered clients can transfer assets between themselves on a no-gain-no-loss basis. If one partner has used their CGT allowance this year and the other has not, the asset can be transferred first, then bedded. If one partner has a fresh ISA allowance and the other does not, the asset can be transferred and bedded into the higher-allowance partner's ISA. These are low-friction, high-leverage moves that are almost always suitable when the client relationship is stable, and almost always missed when the review meeting is with only one partner. The financial advisor meeting notes template has a specific prompt for this case, because it is so easy to overlook.

The Fund-Matching Issue

The 30-day share-matching rule does not apply across the GIA-ISA wrapper boundary, but it can bite if the client also holds the same fund in another GIA (for example, a legacy account at a different platform). If that second GIA has the same ISIN, a disposal in the first GIA and a repurchase in the ISA could technically be matched by HMRC against any sale that happens within 30 days on the second GIA. This is rare but worth checking if the client has multiple GIAs.

The Accumulation-Unit Trap

For funds held as accumulation units in a GIA, the client has been paying income tax on notional distributions and building up "equalisation" adjustments over years, which complicates the cost-basis calculation. The platform's own report of "gain on disposal" is sometimes wrong, because it does not always account correctly for the accumulated-income adjustments. Advisers running bed and ISA on long-held accumulation units should either verify the cost basis manually or delegate to a tax accountant for any significant holding. For a wider discussion of how to build this kind of adjustment into cash flow modelling, see our cash flow modelling guide.

How Heavenly Fits Into the Workflow

Heavenly records the client review meeting where the bed and ISA decision is made, transcribes the adviser-client conversation, and structures the notes so the "alternatives considered" and "client's preference" items are captured verbatim rather than reconstructed afterwards. That matters for bed and ISA specifically because the decision is nuanced, the quantitative case is unavoidably approximate, and the FOS view of suitability leans heavily on whether the client actually understood the trade-off at the time.

Advisers using Heavenly typically ship a review meeting with a bed and ISA decision into a structured file in under six minutes after the call ends, including the tax-year context, the quantified CGT case, and the client's preferences on splitting or running in one go. That is six minutes instead of the forty-plus that reconstructing a decent file note usually takes.

If you would like to see how the meeting-notes workflow handles tax-year decisions end to end, book a demo and we will run through a sample review with the bed and ISA step in place. Good bed and ISA advice is not hard to give. It is hard to evidence. Heavenly makes the evidence the easy bit.