A fact find is the structured discovery meeting an adviser runs to gather everything required to give suitable advice: hard financial facts, soft personal context, capacity for loss, attitude to risk, knowledge and experience, and an assessment of vulnerability. Done well, it is the most valuable hour an adviser spends with a new client. Done badly, it is form-filling: the adviser reading questions off a sheet, the client answering in monosyllables, and the resulting case file neither suitable nor defensible. The difference between the two has very little to do with the form template and almost everything to do with how the meeting is run.

This guide is the practical 2026 playbook for UK financial advisers running fact-find meetings under COBS 9.2 and Consumer Duty PRIN 2A. It covers the six sections every modern fact find must cover, the meeting flow that produces real intelligence rather than checkbox compliance, the failure modes that come up in suitability reviews, and what changes when you treat the fact find as the start of an ongoing intelligence file rather than a one-time intake form. If you want every soft fact, off-hand goal, and unprompted vulnerability cue to make it from the meeting into the case file automatically rather than depending on what you remembered to write up afterwards, Heavenly is built for exactly that. The rest of this piece is the technical content.

What a Fact Find Actually Is

The fact find is the regulatory and practical foundation of suitable advice. It is the moment the adviser converts a stranger's life into the structured case file from which a recommendation can be defended. Three things make a fact find different from any other client conversation:

- It produces a written record on which suitability rests. Every recommendation in the subsequent suitability report should be traceable to a finding in the fact find. If a recommendation cannot be tied back, the question becomes: on what basis was it made.

- It is the regulatory point at which "know your client" is established. COBS 9.2 (or COBS 9A.2 for MiFID II business) requires the firm to obtain the necessary information to assess suitability. Consumer Duty PRIN 2A raises that bar: the firm must understand the client well enough to deliver good outcomes across products, price, communication, and support.

- It is the most data-rich hour the adviser will spend with the client all year. Every subsequent meeting refers back to it. The annual review verifies its assumptions. The replanning event resets it. A poorly captured fact find compounds error across years.

A fact find is not the same as the application paperwork. The application is the form the client signs to open an account. The fact find is the intelligence file the firm builds about the client. Conflating the two produces fact finds that look like application forms (basic identity, basic income, signature) and that fail the suitability test the moment a recommendation needs defending.

The Six Sections of a Modern Fact Find

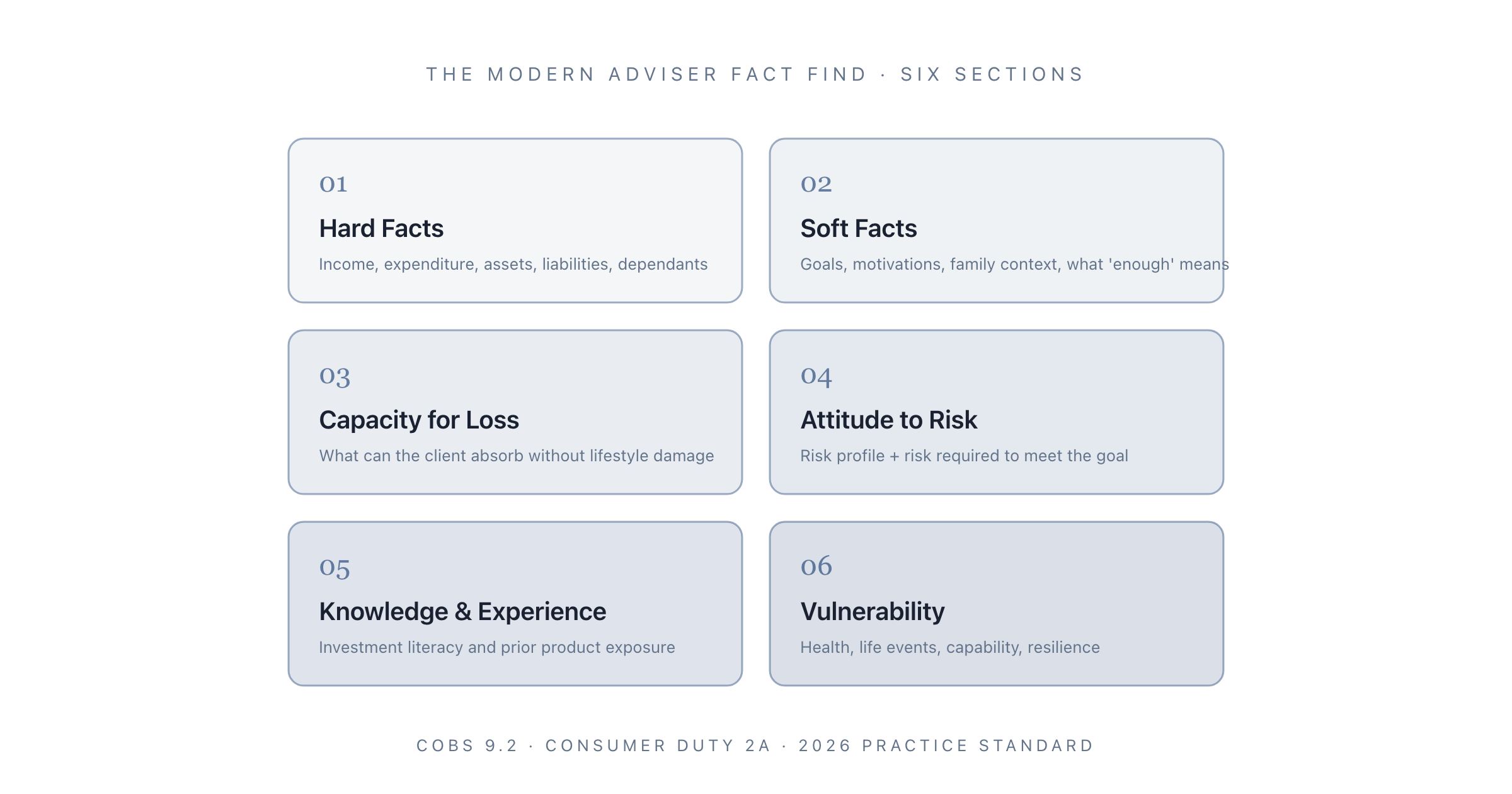

A 2026-compliant fact find covers six sections. Older fact-find templates cluster the first four (hard facts, soft facts, capacity for loss, attitude to risk) and treat knowledge and experience and vulnerability as compliance afterthoughts. Under Consumer Duty, all six are core. The depth on each section is calibrated to the complexity of the client and the products being recommended, but none of the six can be skipped.

1. Hard Facts

The numerical and structural facts of the client's financial life. Income and its stability, expenditure and its breakdown, assets (investable, illiquid, pension, property), liabilities (mortgage, debt, credit), dependants, employment status, contractual benefits, state benefits, expected inheritances, expected liabilities (school fees, care costs, divorce). Five things differentiate a strong hard-facts capture from a weak one:

- Net not gross. Take-home income, after-tax investable surplus. Gross income alone tells you almost nothing.

- Granularity on expenditure. "Approximately £4,000 per month" is a guess. A breakdown into fixed (mortgage, utilities, school fees), discretionary (food, travel, entertainment), and one-off (holidays, replacement car) is the basis of any cash-flow plan.

- Liabilities including timing. A £200,000 mortgage with five years left is a different planning problem from a £200,000 mortgage with twenty years left. Capture the term, not just the balance.

- Pension as both an asset and a constraint. Total fund value, scheme type (DB / DC), accrual rate or contribution level, normal retirement age, transfer status if relevant.

- Assets the client does not think of as assets. Property in a parent's estate, a stake in a family business, a forgotten employer share scheme. Probe specifically.

The hard facts section is the easiest to do mechanically and the easiest to do badly. The adviser who reads the questions in order produces a column of numbers. The adviser who follows the trail of each answer produces a map.

2. Soft Facts

The qualitative context that turns hard numbers into a planning brief. What does the client want from this meeting, this advice relationship, the next ten years of their life. What does "enough" mean to them. What are they worried about that they have not put into words. Who else is involved in the decision (a spouse, a child, a previous adviser, an accountant). What has prompted the conversation now.

Soft facts are where Consumer Duty Outcome 3 (Consumer Understanding) bites hardest. If the soft facts are thin, the suitability report ends up framed in product terms ("a balanced multi-asset fund offering exposure to global equities and fixed income") rather than client terms ("a portfolio that funds your retirement income from age 62 with a margin of safety against a 25 percent market drop"). The product framing satisfies the rules. The client framing satisfies the duty.

The hardest part of capturing soft facts is the silence. Most clients do not articulate their goals on the first ask. The adviser has to be willing to leave space for the second and third sentences, which contain the real material. The classic technique is the follow-up: "And what would that mean for you?" repeated until the client lands on something concrete. "I want to retire at 60" becomes "I want to retire at 60 because I watched my father work until 67 and die at 71 and I am not doing that". The second sentence is the one the suitability report will need.

3. Capacity for Loss

What the client can afford to lose without their lifestyle, plans, or financial security being damaged. Capacity for loss is a different question to attitude to risk and the FCA has been explicit that the two cannot be conflated. A client who is comfortable with risk (high ATR) but whose pension fund is the only resource available to fund retirement (low capacity for loss) is in a position where the adviser has to manage the gap.

Three numerical anchors help capture capacity for loss in a defensible way:

- Essential expenditure floor. What is the minimum monthly income the household needs to maintain its current standard of living? Below this number is "lifestyle damage".

- Time horizon to drawdown. When will the funds be needed? Short-horizon money has a much smaller drawdown tolerance than long-horizon money.

- Backstop assets. What other resources exist if the recommendation underperforms? An emergency fund, an unencumbered home, a partner's pension, a continuing income stream.

A capacity-for-loss assessment that produces a single sentence ("client has moderate capacity for loss") is doing the bare minimum. A capacity-for-loss assessment that produces a numerical floor, a time horizon, and a list of backstops is the one that survives a suitability review.

4. Attitude to Risk

Risk profile, risk required to meet the goal, and the tolerance/capacity gap. Three things matter beyond the questionnaire score.

- The questionnaire is a starting point, not the conclusion. Most ATR questionnaires produce a 1 to 10 score. The score is useful as an anchor for the conversation that follows, not as a substitute for it. The adviser's job is to test the score with scenarios. "If the portfolio fell 25 percent in 2027, what would you do?" The answer to that question is more diagnostic than the questionnaire result.

- Risk required vs risk tolerated. The risk needed to achieve the client's goal may be higher than the risk the client is comfortable with. That gap is the most important single output of the ATR section. It informs the suitability conversation: either the goal is rescaled, or the time horizon is extended, or the contributions are increased, or the client agrees to take more risk than their tolerance suggests with an acknowledgement of why.

- Couple cases. Two-client households often have meaningfully different risk attitudes. A blended ATR is not a substitute for two separate assessments. The household plan has to handle the divergence rather than averaging it.

Capturing the rationale for the final agreed risk profile, not just the score, is what makes the ATR section defensible. "Client scored 6 on the questionnaire. After discussion of historical drawdowns, including a worked example of a 30 percent fall and recovery, client confirmed comfort with a 5 to 6 profile, citing the long horizon of the planning goal." That sentence is the suitability anchor. The number alone is not.

5. Knowledge and Experience

What the client already knows about investing, what products they have held, what worked and what did not, where their understanding has gaps. This section governs both the depth of explanation in the suitability report and the type of products that can be recommended.

A retail client with no prior investment experience is a different recommendation universe to a professional whose career is in finance. The fact find does not need to gatekeep based on the answer; it needs to surface the level so the adviser can pitch the suitability report and the ongoing client communications appropriately. Consumer Duty Outcome 3 (Consumer Understanding) is heavily informed by the knowledge-and-experience section: the firm cannot deliver communications that enable decisions if it does not know where the client starts.

Specific things to capture: prior portfolios held (and where they sit now), self-directed investing history (Vantage, AJ Bell, etc.), professional financial qualifications, prior receipt of advice from another firm and the reason for changing, and any product categories the client has had a bad experience with. The last category is the most under-captured and the most useful.

6. Vulnerability

The FCA's vulnerability framework identifies four drivers: health, life events, capability, and resilience. A 2026 fact find captures vulnerability across all four, not just the headline question of whether the client identifies as vulnerable.

- Health. Physical or mental health conditions that affect the ability to engage with financial decisions. Bereavement (recent or anticipated), terminal illness, cognitive decline, depression, anxiety. Probing this section requires care; the goal is not a diagnostic interview but a record of factors that may affect the adviser's communication and decision-making support.

- Life events. Divorce, widowhood, redundancy, sale of a business, expected inheritance, expected payout from a personal injury claim. Any event that disrupts the client's normal financial baseline.

- Capability. Numeracy, literacy, language, digital access. Where any of these is constrained, the adviser's communication has to adapt.

- Resilience. Whether a financial shock would push the client into crisis. Linked to but distinct from capacity for loss; a client may have the assets to absorb a loss but not the psychological resilience to remain on plan during one.

The most common failure on vulnerability is to treat it as a yes/no checkbox at the end of the fact find. The 2026 standard is to surface vulnerability cues throughout the meeting and capture them in the relevant section. A client mentioning a recent bereavement during the soft-facts section is also a life-event vulnerability cue. A client who hesitates over the simplest expenditure question may have a numeracy capability cue. The structured fact find captures both.

For the broader Consumer Duty framing of how vulnerability and the other outcomes hang together, the four Consumer Duty outcomes guide covers PRIN 2A in full.

The Meeting Flow That Produces Real Intelligence

A fact find covering six sections in a one-hour meeting is impossible if the adviser reads the form. It is straightforward if the adviser runs the meeting as a conversation that loosely tracks the sections. Three principles distinguish a good fact-find meeting from a bad one.

Open with the soft facts, not the hard facts. Most fact-find templates put hard facts first (basic identity, employment, income). Most strong advisers reverse the order. The conversation about goals, motivation, and family context is the conversation the client wants to have. The hard facts follow naturally from it once the planning brief is established. Asking for income and pension fund value before establishing why the client is in the room is the form-filler's mistake.

Follow the trail. When the client mentions an asset, ask about its history. When they mention a goal, ask what triggered it. When they mention a worry, ask how long it has been on their mind. The fact find is not a linear march through a form. It is a structured drift, with the adviser steering back to uncovered sections as natural breaks appear.

Take notes the client can see. Whether the adviser writes on paper, types on a laptop, or relies on an AI meeting-notes tool, the client should be aware of and comfortable with the recording method. Hidden notes feel like an interrogation. Visible structured capture feels like a professional service.

The duration is typically 90 minutes for a new-client fact find, 45 minutes for a refresh fact find at an annual review. Both are best run with a 15-minute pause partway through; the second half almost always produces material the first half missed.

Six Failure Modes That Show Up in Suitability Reviews

The following six are the most common fact-find weaknesses surfaced in compliance file reviews and post-claim disputes.

- Reading questions off the form. Every answer is short, every section is shallow, the client never warms up. The fact find takes 35 minutes and produces nothing the suitability report can lean on.

- Missing the soft facts entirely. The fact find captures every number but no goal, no motivation, no family context. The suitability report is product-led, not client-led, and Consumer Duty Outcome 3 is exposed.

- Capacity for loss as a one-line summary. "Moderate capacity for loss" without numerical anchors. Survives an undisturbed file. Fails the moment a complaint reaches the FOS.

- ATR captured as a score with no rationale. The questionnaire score is recorded, the discussion that produced the agreed risk profile is not. If the recommendation diverges from the questionnaire score (often appropriately), there is no defensible record of why.

- Vulnerability as a tickbox at the end. A binary "yes / no" with no detail. No record of the four drivers, no commentary on the cues that surfaced during the conversation. Fails the FCA's 2021 vulnerability guidance and the 2024 Consumer Duty integration of it.

- Knowledge and experience treated as a regulatory formality. The form records "experienced investor" or "limited knowledge" with no substantiation. The suitability report writes itself in language inappropriate for the client's actual level.

Each failure mode is fixable in the meeting itself. None of them is fixable retrospectively in the case file once the meeting has happened.

What Changes When the Fact Find Is the Start of an Ongoing File

A modern adviser file is not a static form completed at intake. It is a living intelligence file updated at every meeting. The fact find is the foundation, but the soft facts in particular shift continuously: a goal becomes more concrete after a year, a health concern emerges, a parent's care needs change the inheritance picture. A practice that captures meeting notes in a way that updates the relevant fact-find sections automatically is operating at a different level to one that runs a fresh fact find every five years and treats the intervening meetings as standalone events.

This is the design principle behind Heavenly: every meeting note is structured against the fact-find sections, every change to the client's circumstances is propagated into the case file, and the suitability evidence is current rather than dated. For a typical UK adviser running 80 client households, the time saved is roughly the equivalent of a part-time paraplanner. For the practice review, the difference is the difference between a defensible file and a current file.

The paraplanner article covers the related question of how the fact find feeds into the suitability report and the back-office workflow. The cash flow modelling guide covers how the hard facts and soft facts together drive the financial plan. The fact find sits upstream of both and determines the quality of both.

The Bottom Line

A good fact find is a structured one-hour conversation that produces a defensible suitability foundation, a current vulnerability assessment, and a planning brief the client recognises as their own. A bad fact find is a form, completed under time pressure, that produces enough boxes ticked to file but nothing the adviser can lean on when the client's life shifts.

Three operational changes raise the average practice's fact find quality more than any template redesign:

- Lead with soft facts. Reverse the form order in the meeting if you have to.

- Capture rationale, not just answers. Especially on ATR and capacity for loss.

- Treat the fact find as the start of an ongoing file, not a one-time intake.

If the third point is the one most practices struggle with, it is also the one with the largest compounding return. Every subsequent meeting becomes more useful, every annual review takes less preparation time, and every suitability report is stronger because the intelligence file behind it is current.

For the meeting-notes infrastructure that captures fact-find updates in the background of every client conversation rather than as a separate workflow, Heavenly is built for UK adviser practice. The fact find should be the intelligence file the firm builds across years, not the form the firm completes once and shelves.