Inheritance tax planning for UK clients in the 2026/27 tax year sits at an unusual moment in the regime's history. The post-2024 budget changes have introduced two structural shifts that touch almost every adviser file: the inclusion of unused defined-contribution pensions in IHT from 6 April 2027, and the £1 million combined cap on Business Property Relief and Agricultural Property Relief from 6 April 2026. Each, in isolation, is a meaningful change. Together, they are the most significant adjustment to the UK IHT regime since the residence nil rate band was introduced in 2017.

This guide is the practical playbook for UK financial advisers running IHT planning conversations through the 2026/27 tax year and into the 2027/28 reset. It covers the nil rate band stack, the gifting and exemption rules in their current form, the business and agricultural relief reset, the pensions reset, and the specific client conversations to start now while there is still planning runway. If you run a UK advisory practice and want the IHT-trigger flags to drop out of your client meeting notes automatically, Heavenly threads them into the case file the moment a trust, gift, or pension is mentioned. The rest of this piece is the technical content.

The Inheritance Tax Regime in 2026/27

UK inheritance tax is charged on the estate at death, plus certain lifetime transfers, at 40% on the value above the nil rate band. The headline 40% rate is unchanged. The structure that gets you to a smaller taxable amount has more moving parts than the headline rate suggests.

Five thresholds and reliefs do most of the practical work in any UK estate plan:

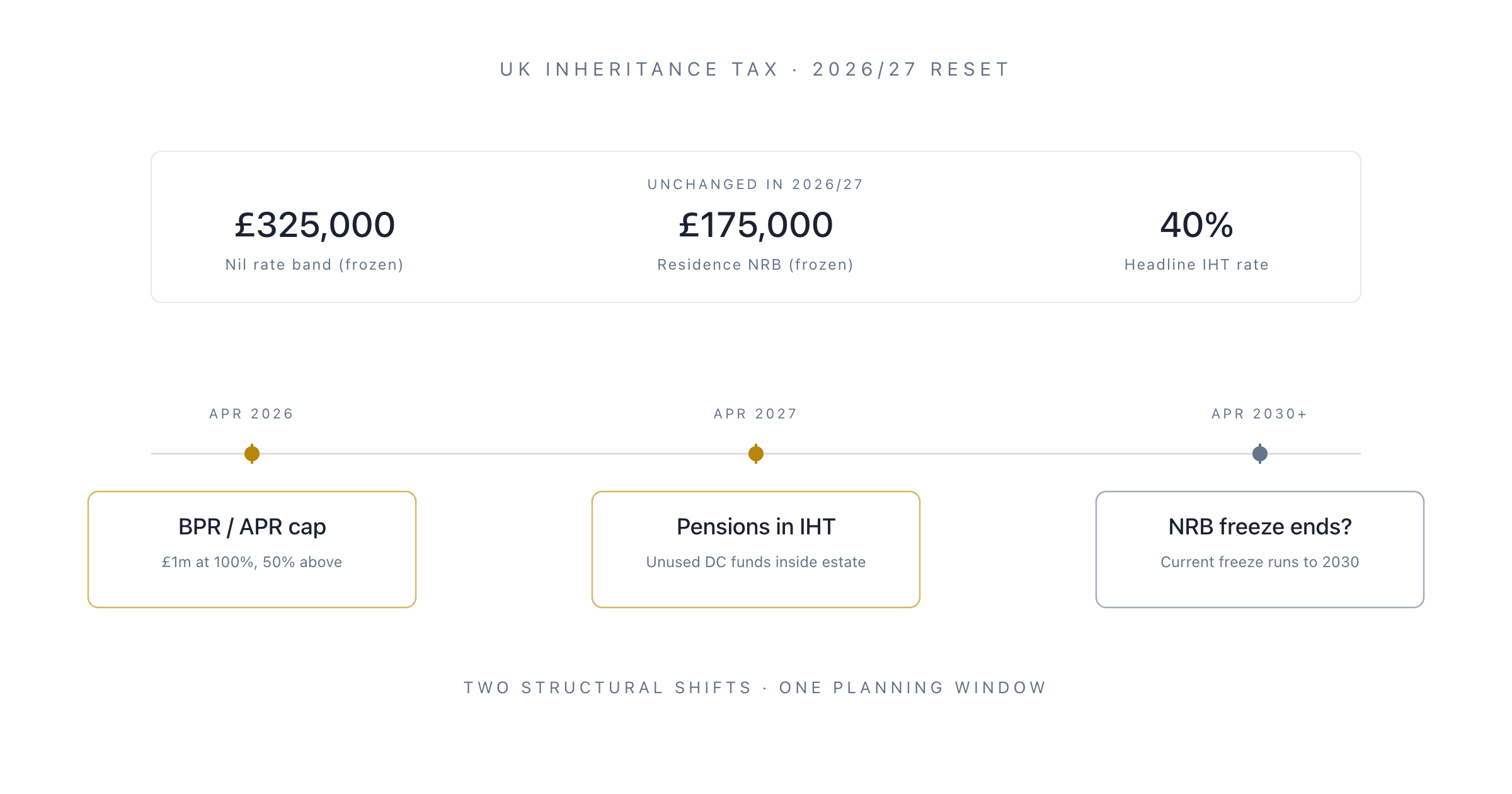

- Nil rate band (NRB): £325,000 per individual, frozen until at least 2030 by the current freeze policy. Transferable between spouses on first death.

- Residence nil rate band (RNRB): Up to £175,000 per individual, available where a qualifying residential property passes to a direct descendant. Tapered above £2 million estates, fully tapered at £2.35 million.

- Spouse exemption: Unlimited transfers between UK-domiciled spouses or civil partners are IHT-free.

- Business Property Relief (BPR) and Agricultural Property Relief (APR): Currently 100% on qualifying business assets and farmland. From 6 April 2026, the combined relief is capped at £1 million per person, with the excess relieved at 50% rather than 100%.

- Pension funds: Currently outside the IHT estate for unused defined-contribution pensions. From 6 April 2027, unused DC pension funds are brought inside the IHT estate.

The interaction between the five is where the planning happens. A married couple with a £2 million estate and a £600,000 home left to children currently has £1 million of allowances (£325,000 + £175,000 each on second death). A couple with the same estate but £1.4 million in DC pensions has, after April 2027, an additional £1.4 million sitting inside the IHT net. A couple with £1.5 million of business assets in a trading company sees, after April 2026, the relief capped at the first £1 million per person (combined £2 million), with a 50% rate on any excess. The 2026/27 conversation is, more than usual, about the lifetime sequencing of those allowances and reliefs.

What Counts Toward the Estate (and What Does Not)

Three categories sit inside the IHT estate at death:

- Property of any kind owned at death. Real property, investments, cash, chattels, business interests not subject to BPR.

- Lifetime gifts within seven years of death. "Potentially exempt transfers" (PETs) become chargeable if the donor dies within seven years of the gift, with taper relief reducing the rate above three years.

- Gifts with reservation of benefit. Gifts where the donor continues to enjoy the asset (the classic example: gifting the family home but continuing to live in it without paying market rent). Treated as still inside the estate.

Three categories do not sit inside the IHT estate:

- Spouse-exempt transfers. Transfers to a UK-domiciled spouse, on death or in lifetime.

- Charity-exempt transfers. Transfers to UK or qualifying overseas charities, plus the 36% reduced rate on the rest of the estate where 10% or more is left to charity.

- Pension funds, currently. Unused DC pension funds remaining in the wrapper at death pass outside the IHT estate. This changes from 6 April 2027.

A fourth category, BPR and APR-relieved property, sits inside the estate but with relief that reduces the chargeable value to nil (currently) or to 50% above the £1 million cap (from April 2026). Property qualifying for BPR includes ordinary shares in unlisted trading companies held for two years, and, in some cases, AIM-listed shares. APR covers agricultural land and buildings used for agricultural purposes.

Get the categorisation right and the rest of the planning conversation has a foundation. Get it wrong (a common error: treating an investment property as BPR-qualifying because it generates rental income) and the plan unravels at probate.

The 2026/27 Reset: What Actually Changes

The two structural shifts in the 2026/27 sequence are different in scale and timing. They affect different kinds of estate. Both need a client conversation now.

April 2026: The £1 Million BPR/APR Cap

From 6 April 2026, BPR and APR are subject to a combined £1 million per individual cap at 100%. Above the cap, the relief drops to 50%, meaning the chargeable estate includes 50% of the value above the cap.

Worked example: a farmer dies on 7 April 2026 owning £2.5 million of agricultural land that previously qualified for 100% APR.

- Pre-April 2026: APR applies at 100% to the full £2.5 million. Chargeable value: £0.

- Post-April 2026: 100% APR on the first £1 million (£1 million chargeable nil). 50% relief on the next £1.5 million (£750,000 chargeable, £750,000 relieved). Chargeable APR-property value: £750,000.

The same arithmetic applies to BPR-qualifying business assets. A founder with a £4 million stake in their unlisted trading company, dying after April 2026, has £1 million at 100% relief and £3 million at 50% relief, leaving £1.5 million chargeable.

The cap is per individual, not per asset, and not per couple. There is no transferable BPR/APR cap between spouses in the way the NRB transfers. Spouses can each have their own £1 million cap if the assets are held separately.

The planning implications:

- Lifetime gifting of qualifying business and agricultural assets to the next generation becomes more attractive than holding them to death. Lifetime gifts of BPR/APR-qualifying property are PETs and get the seven-year clock; the £1 million cap is a death-time check.

- Trust structures for business and agricultural assets need re-modelling. Existing trusts holding qualifying property face the cap on each ten-year periodic charge and on exit charges.

- Asset diversification within a couple's holdings matters. A £2 million BPR-qualifying business held entirely by one spouse loses more than the same business split equally between two spouses.

April 2027: Pensions Inside the IHT Estate

From 6 April 2027, unused defined-contribution pension funds become part of the IHT estate at death. Defined-benefit pensions are largely unaffected. The mechanism is that pension scheme administrators will be required to report unused fund values to HMRC at death, and the inheritance tax payable will be allocated between the estate and the pension. The full operational detail is still being finalised, but the principle is fixed.

Worked example: a client dies on 7 April 2027 with a £600,000 home, £200,000 ISA, £150,000 cash, and £800,000 in a SIPP.

- Pre-April 2027: IHT estate £950,000 (home + ISA + cash). SIPP outside IHT.

- Post-April 2027: IHT estate £1.75 million (home + ISA + cash + SIPP).

The marginal IHT charge from the change is 40% of £800,000, less any allowances. Where the estate already exceeds the available NRB and RNRB stack, the change costs the estate £320,000 in IHT it did not previously face.

The planning implications:

- Pension drawdown sequencing changes. Where a client previously had a reason to draw down ISAs and cash first and leave the pension intact for inheritance, the post-2027 logic flips. Drawing the pension first, paying income tax, and gifting the surplus into life-policy or trust structures becomes part of the conversation.

- Pension death-benefit nominations still matter for income-tax purposes (the recipient pays marginal rate income tax on inherited pension drawdowns from age 75 onwards), but the IHT outcome is now layered on top.

- Spousal pension transfers at death remain spouse-exempt for IHT, but the question of whether to inherit the pension or take it as a lump sum is now a joint income-tax-and-IHT decision.

The April 2027 reset is the single change that touches the largest number of advised UK estates. Almost every client with a pension wrapper above £100,000 has a planning conversation worth having now, while there is gifting and structuring runway.

The Lifetime Gifting Toolkit

The seven-year PET clock has not changed. The annual exemptions and small-gift rules have not changed. What has changed is the relative value of the toolkit because the post-2027 estate is larger for most clients.

The exemptions and reliefs still available in 2026/27:

- Annual exemption: £3,000 per donor per tax year, plus a £3,000 carry-forward from the prior year if unused. £6,000 for a couple.

- Small gifts exemption: £250 per recipient per tax year, unlimited recipients, must not be combined with the annual exemption to the same recipient.

- Wedding and civil partnership gifts: £5,000 from a parent, £2,500 from a grandparent or great-grandparent, £2,500 from one party of the couple to the other, £1,000 from anyone else.

- Normal expenditure out of income: Unlimited if the gifts (a) are made out of income (not capital), (b) are part of the donor's normal expenditure, and (c) leave the donor with sufficient income to maintain their usual standard of living. The most under-used exemption in UK planning. Requires contemporaneous record-keeping of income and expenditure to defend at probate.

- Charitable gifts: Unlimited, both lifetime and on death. Charitable death gifts of 10%+ of the estate trigger the 36% reduced IHT rate on the rest.

- Spouse exemption: Unlimited for UK-domiciled spouses or civil partners.

- Potentially exempt transfers: Lifetime gifts above the exemptions become PETs. After three years, taper relief begins reducing the IHT rate; after seven years, the gift is fully outside the estate.

The under-used items in advisor practice are usually two: the normal expenditure out of income exemption (because it requires the disciplined record-keeping clients resist) and the gifting of pension drawdowns (because the post-2027 framing makes it newly attractive).

A practical sequencing for a client with £150,000 of annual surplus pension drawdown income from age 70:

- Use the £3,000 annual exemption.

- Make wedding gifts where applicable.

- Document the rest as normal expenditure out of income, within the discipline that the gifts are demonstrably from income (a separate gift-tracking ledger, with the income and expenditure analysis attached, kept for the executor at death).

- The remaining drawdown funds can fund whole-of-life policies in trust to cover residual IHT exposure.

That sequencing, run for ten years, can extract £1 million from the estate without using the seven-year clock at all.

The Nil Rate Band Stack Through Each Trigger Event

The two NRB allowances (£325,000 and up to £175,000) have specific transfer and use rules that make them the most reusable allowances in IHT planning.

On first death (married couple):

- Spouse exemption usually means the first death is largely or entirely IHT-free.

- The unused NRB and RNRB transfer to the surviving spouse, expressed as a percentage of the prevailing thresholds at the second death.

- A first-death will using a Nil Rate Band Discretionary Trust (NRBDT) creates a trust up to £325,000 that sits outside the survivor's estate, but at the cost of losing the NRB transferability.

On second death:

- Two NRBs (combined £650,000) and two RNRBs (up to combined £350,000) are available, subject to the RNRB taper for estates above £2 million.

- A direct-descendant gift of qualifying residential property is needed for full RNRB.

- The post-2026 BPR/APR cap and post-2027 pension inclusion both apply here.

On chargeable lifetime transfers:

- Transfers to most discretionary trusts are CLTs (chargeable lifetime transfers), with a 20% lifetime IHT charge above the NRB.

- The NRB is replenished after seven years for further CLTs.

The NRB and RNRB freeze, currently extended to at least 2030, is itself a material planning factor. Each year of the freeze, the real value of the allowance declines with inflation. A £1.5 million estate in 2026 is functionally a £1.7 million estate by 2030, on current Bank of England inflation projections, with no extra allowance to cover the difference.

Trusts in 2026/27 IHT Planning

Discretionary trusts remain the workhorse of UK IHT planning. The core trust mechanics are unchanged in the 2026/27 reset, but two interactions are worth flagging.

First, the Trust Registration Service requires almost every express trust (taxable or not) to register on TRS within 90 days of creation. Any trust used in IHT planning is in scope. Missing the deadline triggers a graduated penalty regime. The TRS workflow needs to be part of every IHT trust conversation.

Second, the BPR/APR cap from April 2026 affects existing trusts holding qualifying business or agricultural property. The cap applies to the trust's relevant property regime charges (the ten-year periodic charge and exit charges) on the trust's qualifying assets, with the £1 million figure applied per settlor's settlements where the rules combine. Existing trusts carrying meaningful BPR/APR-qualifying assets need a re-model in the run-up to April 2026.

The third trust point worth raising in any IHT conversation is the role of cash flow modelling in justifying gifting decisions. A client gifting £500,000 into a discretionary trust needs cash flow evidence that the rest of their resources can support their lifestyle for the rest of their plausible life. Without the cash flow evidence, the gifting decision is exposed at compliance review (specifically against Consumer Duty's understanding outcome) and at probate.

Whole-of-Life Policies as the Backstop

Where an estate has IHT exposure that cannot be fully gifted, structured, or relieved away, a whole-of-life policy in trust is the standard backstop. The policy proceeds pay outside the estate, the trust pays the IHT bill at the second death, and the executors are not forced to liquidate illiquid estate assets to meet the IHT timetable.

The post-2027 reset increases the practical value of the WOL-in-trust route because the average estate's IHT exposure is rising. The economics of a WOL premium versus the expected IHT bill have always been case-by-case; with pensions now inside the estate, the calculation tilts toward more clients having a meaningful policy.

Two operational points: the policy must be written in trust from inception to keep the proceeds outside the estate, and the premiums need to be funded out of normal expenditure where possible to avoid creating their own PET clock.

Domicile, Long-Term Residence, and the 2025 Reform

The April 2025 abolition of the non-domicile regime replaced UK domicile with a long-term residence test for IHT purposes. UK long-term residents (broadly, those who have been UK-resident for ten of the prior twenty tax years) are within scope of UK IHT on worldwide assets. Non-residents with UK assets remain within scope on those UK assets only.

The 2025 reform is now bedded in but still matters for any client with international ties. A returning expat hitting the ten-year mark, an American client whose UK residence approaches the trigger, a client with significant overseas property: each needs the long-term residence position confirmed before the IHT conversation can settle.

The rules differ in detail for trusts created by formerly non-UK-domiciled settlors before April 2025; transitional protections apply but are time-limited.

The Client Conversations to Start Now

The advisor practical work for the 2026/27 sequence has a small number of high-value conversations that should be scheduled with every affected client this tax year.

- For every client with a DC pension above £100,000. The April 2027 pensions reset. Drawdown sequencing, death-benefit nominations, gifting from drawdown surplus.

- For every client with BPR or APR-qualifying assets above £1 million. The April 2026 cap. Lifetime gifting strategy, spousal asset distribution, trust restructuring.

- For every estate above £2 million. The RNRB taper interaction with the post-2027 pension inclusion. Order-of-disposal planning.

- For every couple where one spouse has the bulk of pension assets. Spousal balancing, pension nomination structuring, joint lifetime gifting.

- For every client with overseas connections. Long-term residence position, treaty interaction, double-tax-relief planning.

Each conversation needs structured note-taking to feed into the suitability case file, the cash-flow update, and the gift-tracking ledger. Heavenly handles that thread automatically: the moment the client mentions a trust, a gift, a pension nomination, or a business holding, the relevant IHT-trigger flags are added to the action log so nothing escapes the case file.

What the Playbook Looks Like in Practice

A reasonable 2026/27 IHT-planning workflow for an established advice practice has six stages:

- Triage every client file against the five trigger conditions above. Tag each file with the conditions that apply.

- Schedule the affected reviews through the next twelve months, with priority given to clients facing both the BPR/APR cap and the pension reset.

- Update the cash flow model for every reviewed client to reflect the post-2027 estate position.

- Draft and document the lifetime gifting strategy, normal-expenditure-out-of-income discipline, and any trust restructuring.

- Bring in the policy backstop (WOL in trust) where the residual exposure cannot be planned away.

- Reschedule the annual review to track the seven-year PET clock for any lifetime gifts, the trust ten-year charges, and any further regime changes.

The 2026/27 sequence is unusually busy. It is also the rare moment when the IHT conversation has more planning runway than usual: the pensions reset is a year out, the BPR/APR cap is months out, and there is real time to act before either change crystallises. The advisor practices that triage their book this tax year have the time to put the structuring in place. The ones that wait for the regimes to bite will not.