The UK Trust Registration Service (TRS) is the most under-documented compliance workstream in financial advice. It sits quietly in the background of any adviser file that touches a trust, which is a lot of them, and when it goes wrong it goes wrong in three specific ways: a missed 90-day deadline after a trust is created, a change of trustee or beneficiary that should have triggered an update and did not, or a non-taxable trust that the adviser assumed was out of scope and actually was not after the 2020 and 2022 scope expansions. This guide covers what the TRS is, the current scope after the 5MLD and post-5MLD changes, the exemptions in Schedule 3A, the penalty regime, and the specific workflow an adviser should run inside every client file that touches a trust.

If you run a planning practice and want the TRS checks to drop out of your client meeting notes automatically, Heavenly threads them into the action log the moment a trust is mentioned. The rest of this piece is the technical content.

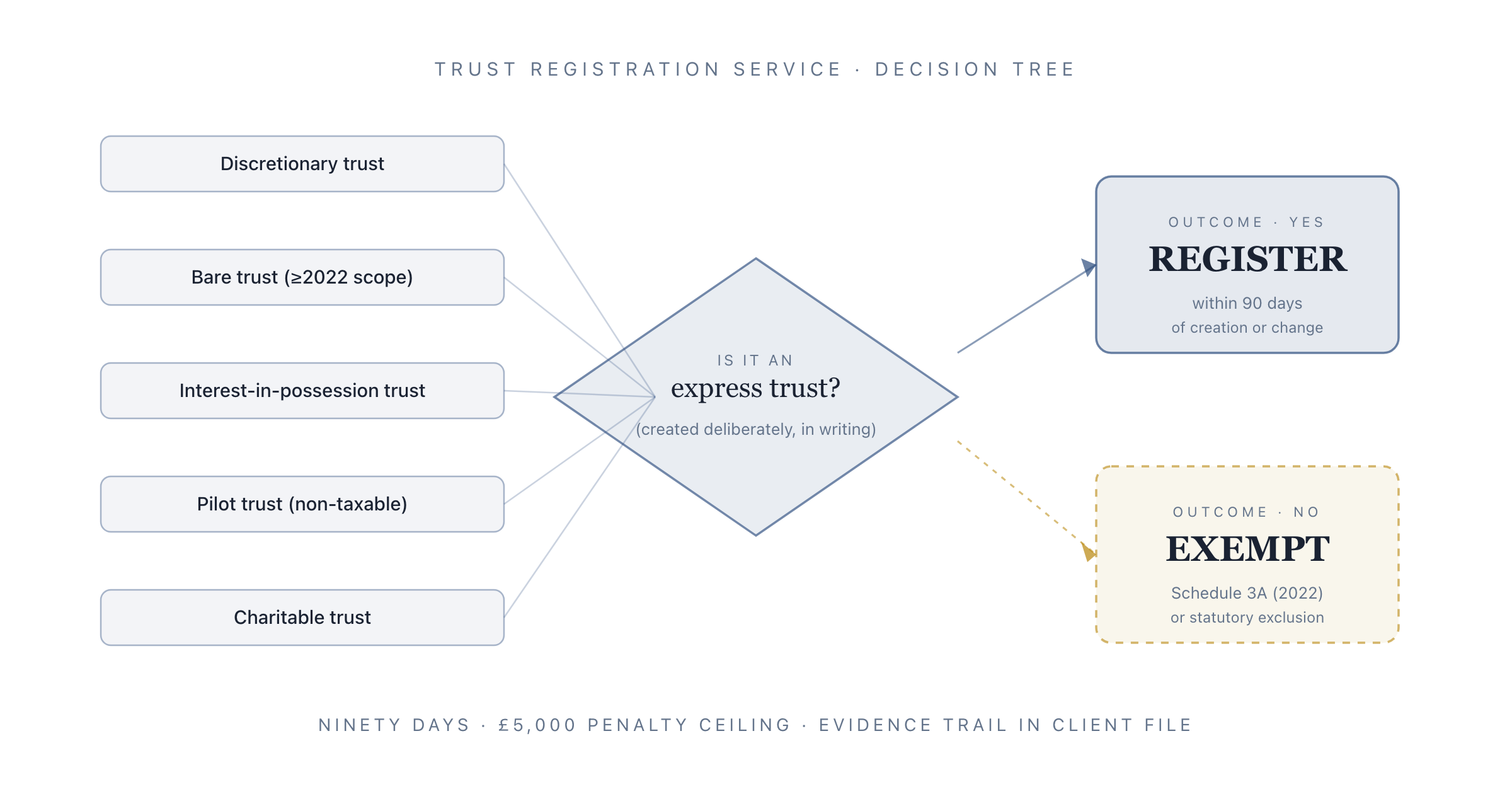

What the Trust Registration Service Actually Is

The Trust Registration Service is HMRC's online register of UK trusts, administered through the Government Gateway and maintained continuously by the trustees (or by an agent acting on the trustees' behalf). It was originally introduced in 2017 to meet the UK's obligations under the 4th Money Laundering Directive (4MLD), which required the UK to keep a central register of taxable trusts. The scope was narrow at that point: trusts had to register only if they had a UK tax liability.

That scope changed twice.

The 5MLD Expansion (1 September 2022)

The 5th Money Laundering Directive (5MLD) was transposed into UK law in 2020 and took effect for TRS purposes on 1 September 2022 via the Money Laundering and Terrorist Financing (Amendment) Regulations 2020. Its headline effect was to extend registration to all UK express trusts, whether or not they had a tax liability, plus most non-UK trusts with a UK nexus. The "express trust" phrase is the most important one in the whole regime: if a trust was deliberately created (rather than arising by operation of law), and was created in writing, it is almost certainly in scope.

The 5MLD expansion is why so many bare trusts, pilot trusts, and other non-taxable arrangements that used to sit outside the TRS suddenly landed inside it from September 2022 onwards.

The Schedule 3A Exemptions

Schedule 3A was added to the Money Laundering Regulations by the 2020 amendment and lists the specific categories of trust that are excluded from TRS registration. The list is closed: if a trust is not in Schedule 3A, and it is an express trust, it must register. Schedule 3A covers a specific, mostly narrow, set of cases:

- Trusts imposed by statute (for example, trusts of land held by co-owners, or the statutory trust under an intestacy).

- Trusts of life policies paying out on death, terminal illness, or permanent disablement, provided the trust was set up at inception of the policy.

- Will trusts wound up within two years of death.

- Pension scheme trusts.

- Charitable trusts regulated in the UK.

- Certain trusts for bereaved minors (Section 71A) and vulnerable beneficiaries under narrow conditions.

- UK registered pilot trusts holding less than £100 (the so-called "£100 rule", tightened post-5MLD).

- Certain co-ownership trusts where legal and beneficial interests are the same.

If the trust does not appear in Schedule 3A, it registers. Advisers should resist the temptation to rely on "but no tax is due" as a reason not to register; the 5MLD expansion severed the registration obligation from the tax obligation.

The 90-Day Rule and What Starts the Clock

The TRS deadline regime has two key timings an adviser should keep in muscle memory.

For Existing Trusts (Pre-2022)

Trusts that existed on 6 October 2020 and came into scope under 5MLD had until 1 September 2022 to register. The grace period has long since passed. Any trust still unregistered now is already late and should be registered immediately, with the reason for lateness noted in the "reasonable excuse" field if applicable.

For New Trusts (From September 2022 Onward)

A new trust must be registered on the TRS within 90 days of the trust being created. "Created" means the date the trust is constituted, which is typically the date of the trust deed, or the date assets are first settled on the trustees, whichever is earlier.

Once registered, the trustees must also keep the register up to date. Any change of trustee, beneficiary, settlor, protector, or beneficial owner must be notified within 90 days of the change. The annual confirmation (a positive "no changes" declaration) is required each year on the anniversary of registration, whether or not anything has changed.

The advice-workflow consequence of the 90-day rule is that any trust created during a planning piece, a new life-assurance-in-trust arrangement, a pilot trust, a bare trust set up for a grandchild, a discretionary trust inside an estate plan, has a hard deadline that starts from the trust deed date and ends exactly twelve weeks and six days later. That is the piece most adviser workflows miss.

Which Trusts an Adviser Actually Encounters

The abstract scope is hard to work with in practice. The specific list of trust types an adviser touches in day-to-day planning is much shorter. The ones that matter, in decreasing order of frequency:

Bare Trusts

The single most common adviser-created trust. Used for gifts to children and grandchildren, for client assets held beneficially but not legally, and for certain investment arrangements. In scope since September 2022, even when non-taxable. The "£100 rule" that used to exclude small bare trusts is tightened: only pre-2016 pilot trusts under £100 are clearly excluded, and even those are worth a second look.

Discretionary Trusts

The backbone of most serious estate planning. Always in scope. If the trust has a UK tax liability (which most do, at some point, even if only from the trustees' own investment income), it registers on the taxable track; otherwise on the non-taxable track.

Interest-in-Possession Trusts

Including the now-less-common interest-in-possession life policies, Immediate Post-Death Interest (IPDI) trusts, and pre-2006 accumulation-and-maintenance trusts with an IIP component. All in scope.

Life Policies Held in Trust

The most important exemption. Life policies paying out on death, terminal illness, or permanent disablement, where the trust was created at inception of the policy and where the only asset is the policy itself, are exempt under Schedule 3A (paragraph 19). But: once the policy pays out, the trust holding the death benefit is not exempt and must register within 90 days of the pay-out. Many advisers miss this second step.

Pilot Trusts

Pre-existing pilot trusts with more than £100 are in scope. Post-5MLD pilot trusts are in scope regardless of value. The "empty trust for later use" no longer sits outside the regime.

Will Trusts

In scope, unless wound up within two years of death (Schedule 3A, paragraph 21). That two-year window is the main operational exemption for probate-era trusts and is worth checking against the estate administration timetable for every will trust adviser sees.

Charitable Trusts

Out of scope if regulated by the Charity Commission (or Scottish/NI equivalents). Advisers working with trustees of UK charitable trusts do not need to register on the TRS.

For the deeper piece on how trust work fits into evidence-based adviser compliance, see our Consumer Duty outcomes guide, which explains why the TRS documentation sits in the same file as the Understanding outcome evidence.

The Penalty Regime

HMRC's penalty framework for TRS non-compliance is graduated by intent, not by how late the registration is, which is the opposite of how most tax penalties work.

First-Offence Penalty

For a first-time failure to register or update on time, HMRC will normally issue a nudge letter rather than a penalty. The letter asks the trustees to register or update, and the penalty clock effectively restarts from the nudge. This is the "benign" track.

Non-Deliberate, Non-First-Offence

A trust that has already been nudged, or whose trustees should have known their obligations from earlier practice, faces a penalty of up to £5,000 per trust. The ceiling has been stable since introduction and HMRC guidance suggests penalties at the top of the range are reserved for cases with significant risk factors (high-value trusts, multiple missed updates, signs of avoidance intent).

Deliberate Non-Compliance

A trust where HMRC can show deliberate non-registration, or deliberate failure to update after a known change, moves out of the £5,000 ceiling and into HMRC's general inaccuracy-penalty regime under Schedule 24 FA 2007. Penalties here can reach 100% of any tax at risk, plus reputational consequences for the adviser if they were the responsible agent.

The single-sentence takeaway: the TRS penalty regime is forgiving for first offences and unforgiving for patterns. Advisers who systematically miss updates are exposed far beyond the £5,000 headline.

Building TRS Into the Adviser Workflow

The recurring failure mode across adviser practices is not ignorance of the TRS; it is that the TRS check sits outside the normal client-meeting workflow, and so gets forgotten between meetings. Three practical patterns fix this.

Pattern 1: The Trigger-Based Checklist

Every meeting note should have a structured "trusts changes" section that explicitly asks four questions:

- Was a new trust created or discussed for creation in this meeting?

- Was there a change of trustee, beneficiary, settlor, or protector in any existing trust?

- Was there a material change of trust asset value or composition that might move a non-taxable trust onto the taxable track?

- Has the annual TRS confirmation been filed on any trust whose anniversary falls in the next 90 days?

If any answer is yes, the action log gets an explicit TRS task with a hard 90-day deadline.

Our financial advisor meeting notes template includes this TRS block as a standard section.

Pattern 2: The Trust Register in Every Client File

A one-page trust register at the front of every client file, listing:

- Every trust the client is a settlor, trustee, beneficiary, or protector of.

- The TRS registration status of each (registered, exempt, not yet due).

- The next anniversary confirmation date for each registered trust.

- The adviser's locus (who leads, who supports, who has the Government Gateway credentials).

The register gets reviewed at every annual suitability review, not just when a trust is mentioned. Most adviser TRS failures are by-omission, and a register that appears in every review catches them before they lapse.

Pattern 3: The 90-Day Calendar

Every trust-registration-triggering event (new trust, change of trustee, death of settlor, change of beneficiary, trust wound up) gets a diary entry dated +90 days in the practice's shared calendar. That diary entry is the TRS deadline for that specific event. The adviser does not rely on memory or on HMRC's nudge letter; the calendar holds the deadline and fires a reminder at +60 days.

Most advisers find the calendar approach is the single biggest change they can make. The regulation is a 90-day deadline; the antidote is a 90-day reminder.

Five TRS Mistakes That Show Up Repeatedly

Across the adviser files we work with, the same five TRS failure modes recur:

- "But it is non-taxable." The most common. The scope expanded in 2022. Non-taxability is not an exemption.

- Life policies, post-payout. The in-force policy in trust is exempt. The matured policy in trust is not.

- Bare trusts for children/grandchildren. Particularly where the grandparent settled the trust but the child's parent is the named trustee. In scope.

- Pilot trusts created pre-5MLD. Many were genuinely small and genuinely unused and genuinely in scope now. Worth auditing every long-standing client's pilot trust.

- Missed annual confirmations. Once registered, the trust needs an annual declaration. This is the slow leak, and the one most visible in HMRC's nudge letters in 2025/26.

Every one of these is catchable by the three-pattern workflow above, and not catchable by relying on memory.

What the Client File Needs to Show

For Consumer Duty evidence purposes, and for defensibility if HMRC ever queries a registration, the adviser file should be able to show, for every trust the client touches:

- A note that the TRS scope question was asked, with the date and the answer.

- If in scope, the registration confirmation (the UTR or the Unique Reference Number, the date of registration, and who filed it).

- If exempt, the specific Schedule 3A paragraph relied on, with a one-line note of the reasoning.

- The next action date (annual confirmation due, change-of-trustee notification due, etc.).

- The client's sign-off that they understand their ongoing obligations as trustee, settlor, or beneficial owner.

Evidence of the ask and the decision is at least as important as evidence of the filing. HMRC's nudge letter asks for both.

If you want to bring that evidence trail into the client-meeting workflow automatically, Heavenly threads TRS checks into your action log the moment a trust is mentioned in the conversation, which is usually the first point at which the 90-day clock might start.

Related Adviser Guides

The TRS sits next to three other compliance workstreams we have written about:

- Cash flow modelling for financial advisers covers the planning context in which many of these trusts are created.

- Consumer Duty outcomes covers the Understanding and Products outcomes that TRS documentation supports.

- Bed and ISA covers the year-round housekeeping that often sits alongside a trust planning piece.

The TRS is not glamorous. It is, however, one of the small set of regimes where the penalty for getting it quietly wrong is larger than the penalty for getting a headline piece of advice visibly wrong. Built into the meeting note, the client file, and the 90-day calendar, it becomes a background hum. Left outside, it becomes a late-spring surprise.